Several Republicans — including presidential candidates Marco Rubio, Jeb Bush and Carly Fiorina — have claimed that business deaths outnumber business births in the U.S. That was accurate for individual firms for 2009 to 2011, in the wake of the Great Recession, but no longer.

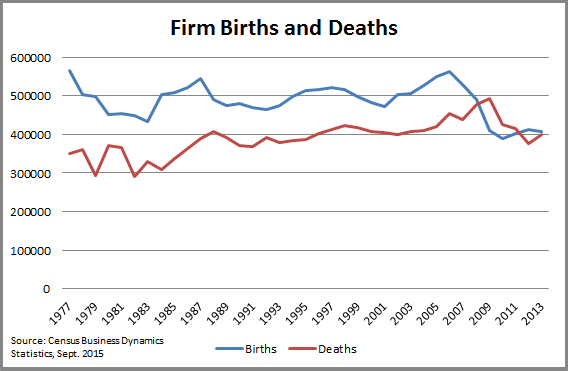

According to the Census Bureau’s September 2015 release of these figures, firm births outnumbered deaths in 2012. And the same goes for 2013.

During the CNBC Republican presidential debate on Oct. 28, three candidates made a version of the claim about business deaths:

- Sen. Rubio said, “You have small businesses in America that are struggling. For the first time in 35 years, we have more businesses closing than starting.”

- Former Florida Gov. Bush claimed, “You think about the regulatory cost and the tax cost — that’s why small businesses are closing, rather than being formed in our country right now.”

- Former Hewlett-Packard CEO Fiorina said that the U.S. has “400,000 small businesses forming every year” and “470,000 going out of business every year. And why? They cite Obamacare.” (Those numbers are close to what Census says was the case in 2009, a year before the Affordable Care Act was even signed into law.)

The source of this claim is a Brookings Institution report from May 2014 titled “Declining Business Dynamism in the United States,” which found that “business deaths now exceed business births for the first time in the thirty-plus-year history of our data.” That’s according to data from the Census Bureau’s Business Dynamics Statistics through 2011. The numbers showed that firm exits outnumbered firm entries in 2009 for the first time since this information was collected in the late 1970s. That was also the case for 2010 and 2011.

The Brookings report looked at “firm” startups and closings, rather than “establishments,” which Census also measures. Firms are individual businesses, while establishments include multiple outlets for existing firms. The Brookings report specifically discussed entrepreneurship, which is why it used the numbers for firms. “The distinction between a new Chase Bank branch opening in your neighborhood versus a brand new community bank is critical — particularly when studying entrepreneurship,” Ian Hathaway, one of the authors of the report, told us via email in May, when we first looked at this claim.

Hathaway also sent us a chart with what was then the most recent data from Census, released in September 2014, that showed firm deaths in 2012 (424,864) still outnumbered births (410,001). That’s a difference of 14,863, and the figures showed that the gap had been narrowing each year since deaths first outnumbered births by 90,670 in 2009. We, in fact, cited those numbers in writing about Fiorina’s claim in the Oct. 28 debate.

But, it turns out, Census had released new numbers for 2013 in September of this year. And in doing so, it revised its figures for past years. The latest statistics now show that in 2012, firm births (411,252) were higher than firm deaths (375,192) by 36,060.

And the same held true for 2013, when births outnumbered deaths by 5,666. We can expect that figure to be revised, too, when Census releases new figures in the future. (To see firm births, look at the firm age tables for those age zero.)

But the latest numbers show that more firms are opening than closing, making this GOP talking point now false.

Why would the Census numbers for 2012 change, from about 15,000 more firm deaths in last year’s release to now about 36,000 more births? Census explains that the figures for business entry and exits take multiple years into consideration. They’re estimates. So when data from another year become available, that affects the previous years’ numbers. (That 90,000-plus gap in 2009 has been revised as well, down to nearly 85,000.)

Census Bureau, Business Dynamics Statistics data page: The BDS uses longitudinal information on firms and establishments to generate measures of business dynamics and job flows. Since information from multiple years is used to produce a statistic for any given year, having more years of data surrounding the year in question improves the quantity and quality of information used to generate the statistics. Thus, less information is available to generate the last year(s) of any given BDS release. Measures of job flows from firm and establishment births are especially sensitive to this source of measurement error and accordingly are more likely to be revised in subsequent releases.

We spoke with Ronald Davis, survey statistician with the Census Bureau’s Center for Economic Studies, who told us: “The number of the last year can change by a good amount when the next year’s data come along.”

On an FAQ page, Census further explains that it adjusts the data for outliers or anomalies. It says that certain entry/exit data may be deemed to be not credible, so they are excluded. For example: “An establishment might fail to report one year; this should not be treated as an exit followed by an entry.”

Davis also explained that while total firms are a “simple count” of what is in the data, the entry and exit data are “adjusted by code that looks for things that should be excluded from the flows.”

The Brookings report indicated that the deaths-outnumber-births trend may in fact reverse, saying in its conclusion: “To be sure, three years have passed since our latest data were collected in March 2011, so it’s entirely possible that some of these negative trends have reversed—or at least stabilized — since then.”

That’s exactly what has happened.

As for why firm deaths would have outnumbered births from 2009 to 2011, Brookings didn’t determine causes, but said the trend matched that of business consolidation in the country. “Our findings stop short of demonstrating why these trends are occurring and perhaps more importantly, what can be done about it,” the report said. “But it is clear that these trends fit into a larger narrative of business consolidation occurring in the U.S. economy — whatever the reason, older and larger businesses are doing better relative to younger and smaller ones.”

Looking at the firm birth and death rates — as opposed to the sheer numbers — shows that what Brookings found was part of a long-term trend. The death rate has hovered around 9 percent for decades, while the firm birth rate has fallen. It was 15 percent in 1978, 10 percent in 1999, and down to 8 percent in 2011, according to Brookings’ calculations.

Hathaway coauthored another paper, for the Federal Reserve Bank of Cleveland, in August 2014 that said there had been a shift away from brand-new businesses toward new outlets of existing businesses, a trend that many Americans may have seen in their own communities.

“The Shifting Source of New Business Establishments and New Jobs,” Aug. 21, 2014: We find that while new firms have been forming at a slower pace over the past 33 years and creating fewer jobs, there has been a simultaneous rise in the number of new establishments opened by existing businesses (which we will call new outlets). … Markets that used to be served by independent entrepreneurs creating businesses are now increasingly being served by the expansion of existing businesses.

This claim has been popular among Republicans, and not just those running for president. Rep. Jeb Hensarling of Texas used the deaths-outnumber-births claim in the GOP weekly radio address in July — attributing the situation to the Dodd-Frank Wall Street Reform and Consumer Protection Act and other business regulation. And the House Republican Conference made the same claim in a March online post titled “Live Long and Prosper — Unless You’re a Small Business.”

Both of those claims were made when the available Census data still supported them. But the House Republican Conference post remains on the website, even though it’s now incorrect. It says that “each year under the Obama Administration, more businesses have shut their doors than opened them,” and that hasn’t been true for individual firms since 2011.