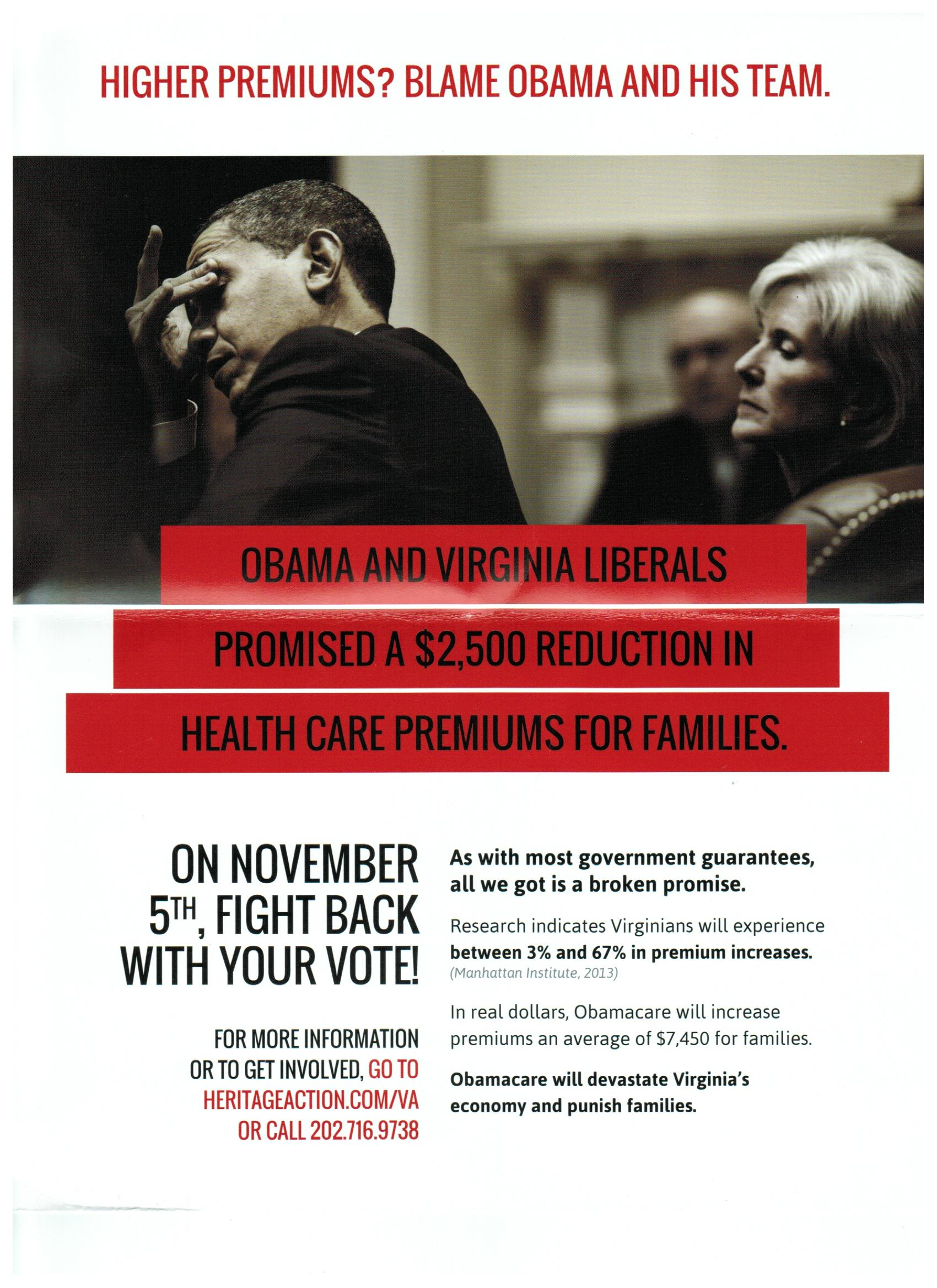

In a mailer to Virginia voters, the conservative Heritage Action calls out President Obama for breaking his promise to save families up to $2,500 in premiums per year under his health care overhaul. But the group makes its own misleading claims about premiums in the process.

- The mailer falsely claims “Obamacare will increase premiums an average of $7,450 for families.” That’s the increase in national health care spending attributable to the law for every four people over nine years — as 30 million uninsured Americans gain coverage. It’s not an average annual premium increase.

- The mailer also wrongly says “Virginians will experience between 3% and 67% in premium increases.” The study it cites actually said premium changes would range from a decrease of 19 percent to an increase of 67 percent. And the estimates are only for the individual market, where 5 percent of Virginians buy insurance, and do not account for subsidies that many will receive.

Heritage Action, a 501(c)4 arm of the conservative Heritage Foundation think tank, starts off by saying, “Obama and Virginia liberals promised a $2,500 reduction in health care premiums for families.” And it goes on to falsely say: “In real dollars, Obamacare will increase premiums an average of $7,450 for families.” That figure comes from a Forbes contributor who calculated the per-capita amount of the increase in health care spending over nine years because of the Affordable Care Act and then multiplied it by four.

It’s a nine-year figure, compared with Obama’s $2,500 one-year figure. Neither of the numbers pertains only to premiums — despite what then-candidate Obama said — and they’re both based on a loose definition of “average family.”

All of those points are made clear by the Forbes contributor who calculated the $7,450 number.

Forbes contributor Chris Conover, a research scholar at the Center for Health Policy & Inequalities Research at Duke University and an adjunct scholar at the conservative American Enterprise Institute, debunked Obama’s campaign promise in a September opinion piece by pointing out that the Centers for Medicare & Medicaid Services estimated that the Affordable Care Act would increase total national health care expenditures from 2012 to 2022 by about $621 billion.

CMS, National Health Expenditure Projections, 2012-2022: By 2022, the ACA is projected to reduce the number of uninsured people by 30 million, add approximately 0.1 percentage-point to average annual health spending growth over the full projection period, and increase cumulative health spending by roughly $621 billion.

National health expenditures include all national spending, from individuals, the government, businesses and insurers. Conover took CMS’ projected increase in national spending due to the ACA for 2014 to 2022, divided that by the projected U.S. population and then multiplied by four to get $7,450. That would be roughly $828 per every four people in the U.S. per year.

“Simplistic?” Conover writes. “Maybe, but so too was the President’s campaign promise. And this approach allows us to see just how badly that promise fell short of the mark.”

It is indeed the same simplistic calculation that the Obama campaign used to come up with its figure on savings. We first questioned Obama’s claim five years ago. He said on the campaign trail in 2008 that his health plan would “lower premiums by up to $2,500 for a typical family per year,” a prediction we called “overly optimistic” and “misleading.” More than half of his projected savings would come from widespread use of electronic health records, his camp said, and he’d get there by the end of his first term, a claim one expert we consulted called “pie in the sky.”

We also explained the “bit of misleading math” the campaign used: It divided an estimate for national health care savings by the U.S. population and, as an Obama adviser told us, “consider[ed] a 4 person family.” The president said he would “lower premiums,” but the Obama camp was counting on trickle-down savings that would affect families in the form of reduced taxes, higher wages or lower premiums. As we said at the time: “Obama claims families will save $2,500 under his plan, but they won’t see at least some of those savings directly in the form of lower premiums. And they may not see them indirectly either.”

Obama was talking about a reduction in health care spending compared with what would have happened without his health plan — not a straight reduction, though he didn’t explain that in his comments.

In 2009, before health care legislation had taken shape in Congress, Obama offered a new version of the claim, saying “comprehensive reform,” plus some effort to reduce costs from labor unions, and insurance, drug and medical industries, “could save families $2,500 in the coming years — $2,500 per family.” We called it “still optimistic.” When experts told us the big 9 percent jump in employer-sponsored family premiums in 2011 was primarily due to rising medical costs — with 1 percent to 3 percent caused by the Affordable Care Act — we pointed out that an increase still wasn’t a decrease. And in 2012, we dissected a new shaky White House claim that “[f]amilies who purchase private health insurance through state-based exchanges could save up to $2,300 on their health care each year.”

We haven’t heard the president continue to make the $2,500-in-savings claim recently. When Republican presidential candidate Mitt Romney resurrected the claim in the first presidential debate last year, Obama only said “the fact of the matter is that when Obamacare is fully implemented, we’re going to be in a position to show that costs are going down.”

CMS doesn’t expect that to happen through 2022. But that’s no justification for Heritage Action to foist more misleading claims on Virginia voters.

Just as the president’s figure includes indirect savings, Conover’s $7,450 figure includes indirect costs, spending by businesses and insurers that are ultimately passed down to Americans in some form. Conover never presented the figure as an estimate on premium costs, as the mailer claims.

Heritage’s wording leaves the impression that families with insurance now would pay $7,450 more in premiums. That’s not the case at all.

We asked Conover how he felt about his figure being used in this way. He said the “way the number was used was sort of misleading in the particulars” — he didn’t say it was a premium increase, for instance, and it was over nine years, not one. The mailer was “a little bit sloppy in how they’ve proven their case.”

“But,” Conover said, “I think it’s very legitimate to point out that the promise was broken.”

We have no argument with that last point, but we’d offer there are accurate ways of doing so.

Not So ‘Typical’

The $7,450 figure is spreading. An ad from Republican Ken Cuccinelli in the Virginia governor’s race says that “his opponent, Terry McAuliffe supported the Affordable Care Act, “costing middle class families thousands” as a graphic is shown saying “$7,450 for a typical family.” But there’s nothing “typical” about lumping together every four people in the U.S.

Similarly, in an ad released this week attacking Democratic Sen. Mary Landrieu of Louisiana, the conservative group Americans for Prosperity said “Obamacare will increase health spending by $6,777 for a typical family of four,” which is the $7,450 number in today’s dollars. Neither of these ads gives any time frame for this increase, nor do they mention Obama’s savings claim.

Conover used the word “typical,” mimicking the president’s wording in his 2008 campaign promise. Readers of the column would know that. But viewers of these ads wouldn’t.

Instead, they may think a “typical family” is one that has insurance, and has it through an employer, since that’s where 56 percent of non-elderly Americans get their health care coverage. The vague “typical” is like the label “middle class,” which is also used in the Cuccinelli ad. Most Americans think they are middle class, as we explained before, and politicians often use the term, without defining it.

Readers of Conover’s column can understand why and how he uses the $7,450 figure and draw their own conclusions from it, knowing that this nine-year average would mean more spending for some and less for others, as 30 million of the uninsured gain coverage. But these political messages strip the figure of that context, and, in the case of the Heritage Action mailer, wrongly call it a premium increase to boot.

If we did want to look at how a family’s health care spending would increase, Josh Gordon, policy director of the nonpartisan Concord Coalition, suggests a more relevant figure would be changes in premiums and out-of-pocket costs. “If you wanted to say something about how a family of four’s health care spending will either increase or decrease, you probably should be talking about health care spending in the way that they understand health care spending,” he told us. “Not by dividing some huge number … to create a mythical family of four.”

“It doesn’t say much to say that total health care expenditures are going to grow — when adding 30 million more people,” he added.

Omitting Premium Decreases

The Heritage Action mailer also says: “Research indicates Virginians will experience between 3% and 67% in premium increases.” It attributed the numbers to the Manhattan Institute, a conservative think tank, which did an analysis of premiums under the Affordable Care Act.

But Heritage Action misquotes the study, which actually said the premium change would range from a decrease of 19 percent in price to an increase of 67 percent. Plus, the mailer neglects to say the analysis was only about premiums on the individual market — where about 418,000 Virginians, 5 percent of the state’s population, now purchase their own insurance, according to numbers from the Kaiser Family Foundation.

The Manhattan Institute report compared the lowest cost premiums on the individual market before the exchanges, adjusted for preexisting condition denials or rate hikes, in each state to the lowest cost premiums on the new exchanges. The methodology explains that it included the five least expensive plans on a county basis before the law took effect and those now being sold on statewide exchanges, excluding catastrophic plans, for 27-, 40- and 64-year-old males and females who don’t smoke.

The institute didn’t adjust the level of benefits or coverage of these plans. As we’ve said before, the law requires certain minimum benefits, which many individual market plans don’t meet. Not everyone will take advantage of, or welcome, those expanded benefits, of course, and the study was looking only at the cheapest plans available on the market before and after these regulations kicked in and the exchanges opened.

Using that methodology, it calculated a wide-range of premium changes on the individual market in Virginia — from a 67 percent increase in premiums for 27-year-old males to a 19 percent decrease for males aged 64.

It didn’t include premiums for catastrophic plans, which could offer a cheaper option to those 27-year-olds. Those under age 30 can purchase catastrophic plans, which cover less than 60 percent of the average cost of health care, but these young adults won’t be eligible for subsidies if they choose such a plan.

The lowest cost catastrophic plan we found on HealthCare.gov for a young person living in Fairfax County, Va., outside of Washington, D.C., was $123.93 per month, for example. That’s $58 less than the average of the five lowest cost state plans, $182, as calculated by the Manhattan Institute without catastrophic plans. But it’s higher than the average of the five lowest cost plans before the Affordable Care Act, $109.

The figures used in the Heritage Action mailer also don’t account for subsidies, which the Manhattan Institute estimates will be available to 51 percent of uninsured Virginians, or 606,000 people. Subsidies are available to those earning up to 400 percent of the federal poverty level, which is nearly $46,000 for a single person and about $94,000 for a family of four.

We don’t know what percentage of Virginians who currently buy their own insurance would be eligible for subsidies. The Congressional Budget Office estimated that about 80 percent of all those buying exchange plans would qualify for subsidies.

It is inherently difficult to make general comparisons between old individual market premiums and the exchange plans. The nonpartisan Kaiser Family Foundation said it couldn’t do so in a report it issued on exchange premiums. It said the changes in this market — including minimum benefit requirements and no denial or price variation based on health status — “make direct comparisons of exchange premiums and existing individual market premiums complicated, and doing so would require speculative assumptions and data that are not publicly available.”

As we’ve said several times, some Americans will pay more, some will pay less, depending on several individual factors, including age, health status and where they live. Experts have long said younger, healthier Americans would likely pay more on the individual market, while older or less healthy folks would pay less. And the study supports that.

Again, we wouldn’t fault Heritage Action for criticizing Obama for having promised a premium decrease of $2,500 per family. We’ve done it plenty of times ourselves. But the group attempts a fight-fire-with-fire tactic that presents more spin to voters.

— Lori Robertson